Making Taxes Painless Starts with Clean Accounting

by Magen Smith, CPA

No one wants to pay more in taxes than they should, self-storage owners included. Working hard on your self-storage business every day of the year only to hand over a large check to the government on tax day is painful and unpleasant. However, seeking to minimize taxes smartly should be the goal for every business owner. Spending $60,000 on an unnecessary truck to save only $20,000 in taxes is a waste of $40,000. Too many business owners try to spend money to save taxes. Instead, focus on maximizing tax savings on the money already spent.

Below are some painless suggestions that will help you keep more of your profits this year.

Enter Income Correctly

Making taxes painless starts with having clean accounting records. Many of my clients have saved thousands of dollars in taxes each year simply by recording their income correctly. Income should be entered from the self-storage management system and then reconciled from the bank account. Far too often, all bank deposits are entered as income. These deposits likely include sales tax, security deposits and other potentially non-taxable items. Entering your income using the self-storage management system ensures revenue is entered correctly as rent, late fees, administrative fees, sales tax and so forth. It is also an excellent way to check if all of the money shown as collected in the self-storage management system was actually deposited into the bank account.

There are multiple ways of entering the income from the self- storage management system into the accounting system. Most self-storage management systems provide reports for daily deposits which can be entered into the accounting system. Using a journal entry report from the self-storage management system or integrating directly with your accounting system are two options.

Enter Expenses Correctly

Once the income in your accounting system is correct, add the expense information. Make sure all of the business’s bills and bill payments, payroll information, refund checks written to tenants, payments on bank loans, and owners draw amounts are added into the accounting system.

Excluding reductions in liability or changes in equity, the money spent in your business falls into two buckets: expenses or assets. Common expenses are advertising, dues and subscriptions, office expenses, payroll, repairs and maintenance and utilities.

Assets are items which will be used for years and should be depreciated. When buildings, vehicles, large office furniture, improvements to the building that extend the useful life, or machinery and equipment are purchased, they are shown on the balance sheet as an asset. Each year, depreciation expense is recorded until the asset is fully depreciated.

Depreciation rules constantly change, so it is wise to consult your tax professional to ensure that all assets are properly recorded. A common tax strategy in self storage is cost segregation. Many professionals will perform cost segregation studies to determine if it is a wise investment or not, but the basic strategy is using the useful life of each component to depreciate the asset. This will commonly increase depreciation in the first few years. Be aware, depreciation expense will eventually run out, and taxable income will increase in later years. Consult with your tax professional to determine if cost segregation is best for you.

Review Your Balance Sheet for Errors

Reviewing the balance sheet is an excellent way to save tax money and reduce personal property taxes if your state has them. I consulted with one client who had a building missing on his depreciation schedule for ten years so he missed all the depreciation expenses he could have taken. No one ever thought to determine what was included in the purchase price and it was all coded to land, which isn’t subject to depreciation.

Your tax CPA should be able to provide you with your depreciation schedule. Go through each item and make sure it still exists in the business. Also, look around at the assets and make sure they are on the schedule.

Common items that will appear on a depreciation schedule are buildings, building improvements, parking lot improvements, vehicles, golf carts, computers, office furniture and any machinery the business owns

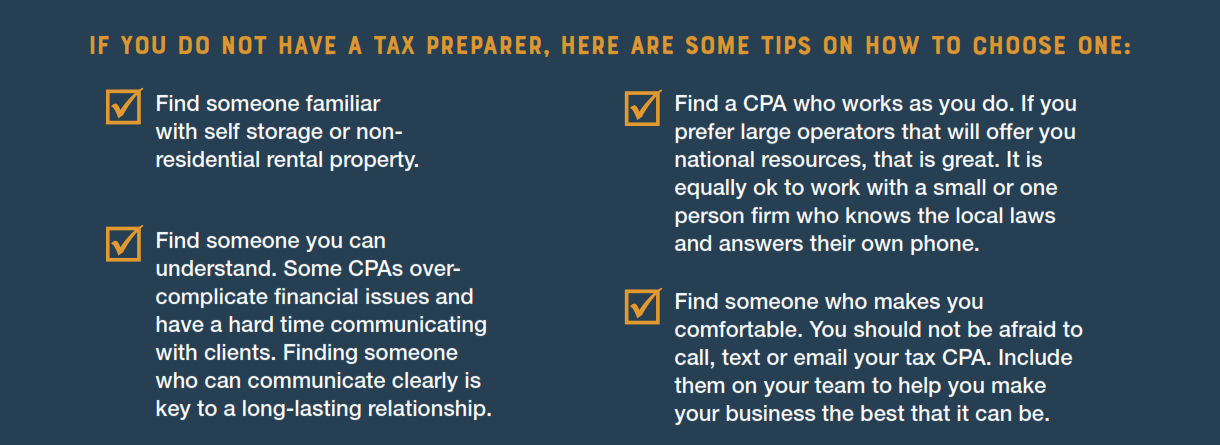

Working With an Accountant

The most painless and comprehensive way to make sure all of the right information is in the accounting system is to have a CPA familiar with self storage handle your accounting.

Once all of the accounting information is properly entered in the accounting system, it is critical that bank and credit card statements be reconciled. It is also wise to tie income numbers back to the self-storage management system to make sure the information is properly recorded. You can certainly do all of this yourself, but using a CPA who is familiar with self storage throughout the year can give you timely, relevant statements which will help grow your business.

Once it is time to prepare taxes, your accountant should provide your tax professional with the year-end statements, along with all supporting documents to make tax filing as painless as possible. Because your tax professional is looking at clean accounting records, he will be less likely to ask you to rummage around for some receipt from 11 months ago that you have misplaced. If the records are well-organized for the tax preparer, he can focus on advising on tax issues and helping plan for the future, instead of doing detailed accounting work.

The best time to save taxes is throughout the year, not right before the filing deadline in April. By that point, it is too late to change the previous year. Meet with your tax CPA in the summer for a mid-year review and again in the fall so they can estimate the taxes that will be owed and give you advice on any last-minute changes to minimize your tax obligation.

Magen Smith started as a self-storage manager and went on to become a licensed CPA. Her CPA firm focuses on self-storage companies by helping them with accounting, getting started in the self-storage industry, raising rates, improving operations and providing audits so they know their business is running properly. She has online courses on revenue management and how to read Sitelink reports available on her website.

Read More Blog Posts »